Most companies don’t start with complex valuation needs because the most important thing is speed when you’re getting a business off the ground.

Automated 409A platforms have made it easier than ever to obtain a compliant valuation quickly and affordably; sometimes even for free. For early-stage startups, this is often the right solution.

But there is a point, often subtle, where automation stops being enough and starts becoming a risk.

This is where companies become what I call: an “Automated Platform Graduate”

What Is an “Automated Platform Graduate”?

An Automated Platform Graduate is a company that has outgrown algorithm-driven 409A valuations due to increasing operational, financial, or structural complexity.

In simple terms:

Your company has evolved faster than the model evaluating it.

These companies typically exhibit:

- Multi-layered capital structures (SAFEs, convertibles, preferred stacks)

- Institutional investor involvement

- Secondary transactions or liquidity events

- Non-linear growth or shifting business models

As discussed in my newsletter, Weapons of Mass Value Creation, valuation is not a static output it evolves alongside a company’s strategy, risk profile, and market positioning.

Why Automated 409A Platforms Work Until They Don’t

Automated platforms are optimized for efficiency and standardization.

They rely on:

- Benchmark datasets

- Predefined volatility assumptions

- Template-based option pricing models

- Limited qualitative overlays

This works well when a company is:

- Early-stage with simple capitalization

- Pre-institutional funding

- Operating within predictable peer benchmarks

However, as companies scale, these assumptions begin to break.

The Core Problem: Standardization vs. Reality

Automation depends on comparability. However, high-growth companies become less comparable over time, not more.

At Objective Investment Banking & Valuation, we frequently see companies whose:

- Growth trajectories diverge from benchmarks

- Strategic positioning is unique

- Risk profiles are misunderstood by generalized models

At that point, valuation becomes less about inputs and more about judgment.

The Hidden Risk: False Precision

One of the most overlooked risks in automated valuations is false precision.

Outputs appear rigorous:

- Clean numbers

- Tight valuation ranges

- Polished reports

But underneath, assumptions may be generalized, inputs may not reflect company-specific realities, and sensitivity to key drivers are often understated.

Precision without context creates confidence without accuracy.

For 409A purposes, this can lead to:

- Mispriced common stock

- Audit challenges

- Disconnects between investor pricing and internal valuation

When Should You “Graduate” from Automation?

Most companies transition too late, so here are some quick and easy inflection points to lookout for:

1. You Raise Institutional Capital

VC involvement increases scrutiny and requires alignment between preferred pricing and common equity valuation. Your equity starts becoming more and more important for talent acquisition and talent retention.

2. Your Capital Structure Becomes Complex

Layered securities may require hybrid approaches, outside models for warrants, or even require scenario-based modeling. Automated comp searches may not yield the right comparables, and DLOMs become a sensitive discussion.

3. You Have Secondary Transactions

Real market signals must be incorporated and sometimes secondary methodologies are needed to support values. Secondary transactions may also need qualitative scrutiny, and the automated platforms do not provide this.

4. You Face Audit or Investor Scrutiny

Auditors expect:

- Transparent assumptions

- Defensible methodologies

- Clear documentation

- Live conversations

They also expect some flexibility and maybe even adjustments, which requires time and effort on the provider’s side to reach a reasonable path forward.

5. You Are Preparing for an Exit

M&A readiness requires valuation frameworks that withstand third-party diligence, and may involve additional methodologies and sensitivities. Automation platforms rarely handle this well.

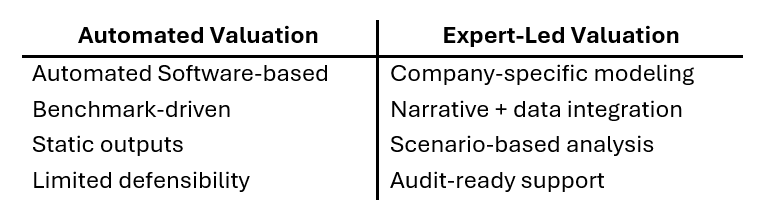

What Changes After Graduation?

Graduating from automation is about upgrading methodology, expertise, and personal guidance.

As I often emphasize in my work advising founders and boards through Objective, valuation is both analytical and use-case driven, and rarely benefits from black and white answers.

Here’s the shift to look out for:

The hidden truth: 409A Is Not Just Compliance, It’s a Signal

Many founders treat 409A valuations as a regulatory requirement. In reality, this analysis functions as much more for all stakeholders, including:

- Employees rely on equity for value credibility and company progress

- Investors rely on valuations for pricing discipline, planning, and progress checks

- Auditors rely on these reports for governance quality and financial reporting match

Increasingly, the 409A is a talent signal. Candidates and employees are actively evaluating what their equity is worth, and whether leadership can clearly explain it. As explored in “The Infamous 409A – Equity Over Cash”, equity only becomes a true motivator when companies can transparently communicate both its current value and future potential.

More broadly, valuation itself becomes a strategic lever. Companies that invest in valuation quality gain an advantage in attracting talent, aligning incentives, and communicating progress to stakeholders, turning 409A from a compliance exercise into a competitive advantage “409A Valuations – Simple Yet Critical”.

Automation primarily optimizes for efficiency. This is fine early on.

However, graduate companies need optimize for credibility, transparency, and the ability to clearly define the purpose of the valuation, apply the appropriate standard of value, and align the analysis with its intended use case.

FAQ: About IRC 409A Valuations and 409A Pricing

What is a 409A valuation?

A 409A valuation is an independent assessment of the fair market value of a private company’s common stock, used to set stock option strike prices in compliance with IRS regulations.

Are automated 409A valuations compliant?

Yes, many automated providers produce IRS-compliant valuations and qualify for the “safe harbor” presumption. However, compliance does not guarantee defensibility under audit or investor scrutiny. As your company grows in complexity, the standard shifts from simply meeting regulatory requirements to being able to clearly justify assumptions, methodologies, and outcomes; something automated approaches may not fully support.

When should I stop using an automated valuation platform?

You should reconsider automated valuation platforms when:

1. You raise venture capital and/or 2. Your capital structure becomes complex or/and 3. You experience rapid or non-linear growth or/and 4. You anticipate audits or liquidity events.

What are the risks of automated 409A valuations?

Automated 409A valuations can introduce risks when they rely on generic assumptions that may not accurately reflect your company’s financials, growth trajectory, or market position. They may also offer limited transparency into the methodology used, making the valuation harder to defend during audits or due diligence.

In some cases, automated valuations can diverge from recent investor pricing or market-based indicators, creating inconsistencies that may raise questions from auditors, investors, or employees. Reduced customization and documentation can also weaken overall audit defensibility.

Do auditors accept automated valuations?

Auditors may accept them for simple, early-stage companies. As complexity increases, they often require more detailed support and expert judgment.

What makes a valuation “defensible”?

A defensible valuation includes: transparent assumptions, appropriate methodologies, company-specific analysis, documentation that can withstand audit and scrutiny.

Does a better 409A valuation reduce risk?

Yes. A high-quality valuation improves: audit outcomes, governance credibility, and/or alignment with investors and stakeholders.

Can a 409A valuation impact fundraising?

Indirectly, yes. Inconsistencies between valuation outputs and financing terms can raise concerns about financial discipline and governance.

How much does a 409A valuation cost?

The cost reflects the complexity of your company’s stage and capital structure, not just the hours involved. At the early end, a simple backsolve for a pre-revenue company starts around $3,500. A standard Option Pricing Method analysis for a Series A or B company typically runs $4,500. More complex engagements, biotech companies, multi-class capital structures, or Series C and beyond, start at $5,500. These ranges are relatively consistent across qualified independent firms; what varies is the depth of analysis, the methodology applied, and whether the resulting report can hold up under auditor scrutiny.

Why did my 409A cost more than the last one?

Usually because your company got more complex. As you raise additional rounds, your cap table accumulates preferred stock with varying liquidation preferences, anti-dilution provisions, and participation rights. Each new layer requires a more rigorous allocation methodology and more detailed documentation to produce a defensible conclusion. A backsolve that was appropriate at the seed stage is no longer sufficient once you have a Series B with meaningful preferences and a growing option pool. The step-up in price reflects a step-up in analytical work and in the credibility of the output.

Meet the Expert

Jordi Pujol has over 15 years of experience in financial modeling and valuation, advising companies and investment firms on financial reporting, tax compliance, and strategic initiatives. He leads the Valuation Advisory Services Group and supports the firm’s national expansion of valuation offerings. Before joining Objective, he was a Senior Manager in EY’s Corporate Finance practice within Strategy and Transactions, focusing on valuation engagements for technology and healthcare clients. His experience spans purchase price allocations, business valuations, goodwill impairment testing, 409A and other compensation-related valuations, intellectual property and intangible asset valuations, and investment holding valuations for private equity and venture capital funds, as well as audit support for public and private entities. Mr. Pujol earned his Bachelor’s degree from Swarthmore College, a Master’s in Finance from EGADE Business School, and an MBA from The Wharton School at the University of Pennsylvania, and he is a CFA charterholder.

Disclosure

This news release is for informational purposes only and does not constitute an offer, invitation or recommendation to buy, sell, subscribe for or issue any securities. While the information provided herein is believed to be accurate and reliable, Objective Capital Partners and BA Securities, LLC make no representations or warranties, expressed or implied, as to the accuracy or completeness of such information. All information contained herein is preliminary, limited and subject to completion, correction or amendment. It should not be construed as investment, legal, or tax advice and may not be reproduced or distributed to any person. Securities and investment banking services are offered through BA Securities, LLC Member FINRA, SIPC. Principals of Objective Capital are Registered Representatives of BA Securities. Objective Capital Partners and BA Securities are separate and unaffiliated entities.